Linda C Turpin

Linda C Turpin

In the 20th century, retirement worked like this: You worked for 40 years, saved five to 10 percent of your paycheck, and then retired on a combination of a pension, Social Security, and spending down the small nest egg you’d set aside.

That’s not how retirement works anymore.

Today, pensions have all but disappeared from the private sector. The purchasing power of Social Security benefits has been shrinking since 2000—30 percent by one report—and there’s no reason to believe that trend won’t continue, given that Social Security is now running a deficit. (1)

All this means that Americans are increasingly on their own for saving, investing, and planning their retirement. That’s daunting enough for someone like me, who gets paid to teach early retirement planning and FIRE tactics. But for the average American, it seems a near impossible task.

Fortunately, saving a nest egg in stocks and bonds and then spending it down in retirement isn’t the only game in town anymore. Americans are increasingly turning to real estate to help with their retirement income.

Here are eight reasons why, and how you can use real estate to not only supplement your retirement income, but also use it to help you retire young.

How Rental Properties Can Supplement Your Retirement Income

1. Ongoing Income with No Loss of Assets

The 20th century model involved gradually selling off stocks and bonds from your nest egg. It made sense: Why force yourself to live only on the dividend and interest income, when you were only going to live for another decade or two after retiring anyway? Whatever was left over when you died would go to the kids, end of story.

I don’t know about you, but I’d like to reach financial independence by 40—or at worst, by my early 40s. But that means being able to live on my investments for a half century or more—a daunting task if your plan involves gradually selling off your assets.

You don’t need to sell your rental properties to produce high-yield income. They’re the golden goose: they lay another golden egg every month, until you slaughter them by selling. You can earn 6 to 15 percent cash-on-cash returns on your rental income, depending on your investing strategy and market. But finding reliable stocks, funds, or bonds that pay 6 to 15 percent yield proves a lot more challenging.

Plus, you have to subtract for inflation from stock and bond returns. More on that momentarily.

It boils down to one massive advantage: When you don’t have to sell off your assets to produce strong monthly income, you don’t have to worry about things like sequence of returns risk or safe withdrawal rates. Because you’re not selling off assets, you don’t have to worry about running out of money.

2. Inflation-Adjusted Returns

Rents not only go up with inflation, they’re a primary driver of inflation. That means your returns inherently adjust to keep pace with inflation, rather than being watered down by it.

In contrast, imagine a one-year bond that pays 4 percent. You earn interest payments all year, then get your initial bond investment back when it matures, so after a year, you have your cash back plus 4 percent.

Except that your money is worth less today than it was a year ago. If inflation ran 2.5 percent that year, then your real return is only 1.5 percent—which is pretty hard to get excited about.

But you raised your rent by 3 percent, meaning that you’re actually earning 0.5 percent higher returns than you did the year before. That makes it far easier to live on your returns from rental properties.

3. Predictable Returns

I’ve written a lot about forecasting cash flow and predicting rental returns, so I won’t belabor the point here. But it’s true: With even modest education and experience, investors can learn how to accurately forecast their returns.

Sure, your take-home profit from each unit bounces around month to month. You might go five months with no irregular expenses, then suddenly have a $500 repair or a month’s vacancy while you advertise the unit for rent.

But in the long-term, these expenses average in extremely predictable ways. So at the end of each year, your returns will look similar. It simply involves discipline—discipline to not put on rose-colored glasses when forecasting returns before buying, and discipline to actually put aside the money for future expenses each month rather than pocketing it all.

4. Leverage

You can leverage other people’s money to build your own portfolio of rental properties. Their money, your assets, and with each one you add to your passive rental income.

New investors tend to take this concept too far, looking for get-rich-quick plans. In my Facebook group for landlords and real estate investors, a woman asked last week how she could buy a rental property with no money down, then added as an afterthought, “Oh, and I’m a mom, so I don’t have any time to put into this—what’s my best option?”

So you don’t have any money to invest, and you don’t have any time to invest. What do you have to invest then?

Rental properties aren’t a free lunch. You do have to invest something, usually both some money and some time. But you don’t have to invest the full purchase price—or even most of it. You can let others cover most of your costs and still come out ahead with positive cash flow.

With each month that goes by, you earn income and you gain equity.

5. Your Net Worth Rises Over Time Rather than Ebbing

Earlier, I touched on the fact that you don’t have to sell off any assets to generate income with rental properties, unlike stocks and bonds. So instead of gradually selling off your nest egg, your net worth actually grows over time.

It grows because your equity in each property grows. That happens through two forces: appreciation and mortgage repayment.

You can’t take appreciation for granted, of course. A sleazy local developer could grease the palms of an equally sleazy local politician to get the road to their new development built—right through your property’s backyard. But most properties do appreciate in value over time.

And your mortgage balance always drops over time, assuming you make your payments. In fact, your tenants actually pay off your mortgages for you. You earn a paycheck every month, your mortgage balance drops, and your property value goes up—win, win, win.

6. Diversification of Asset Types

I love stocks, don’t get me wrong. I invest in a series of index funds every single month, automated through a robo-advisor. (I use Schwab’s Intelligent Portfolio service, which is free with a minimum balance of $5,000.)

But stocks are volatile, which makes it hard to trust them for month-to-month income. One nice thing about real estate markets is they rarely move in sync with the stock market—the housing crisis and subsequent Great Recession proved a particularly salient exception.

Usually, however, housing markets aren’t troubled by stock market corrections. And housing market dips tend to be local events, not the nationwide catastrophe we saw in 2008.

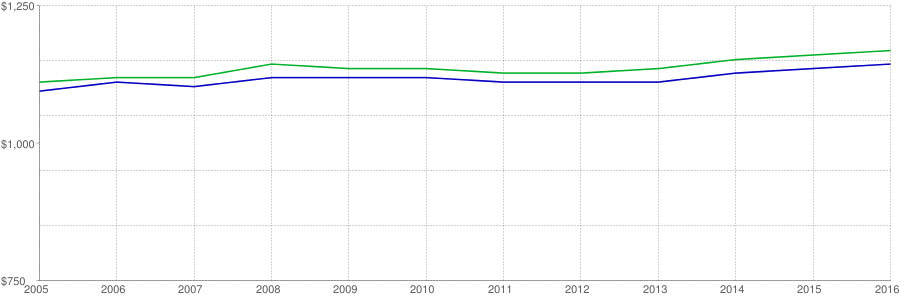

Even when housing prices do dip, rents almost never do (at least on a nationwide level). In the Great Recession, rents simply leveled out for a couple years:

And if you’re living off both rental income and dividends from stocks, you can lean more heavily on one or the other if one has a tough month. If you have a major rental expense that month, you can sell off a few stocks. If the stock market slips, you can hold off for a few extra months on that property upgrade you were thinking about making.

7. Tax Advantages

Every rental property expense is either deductible or depreciable.

Maintenance, property management costs, travel, legal forms, tenant screening reports, insurance, property taxes—all deductible. Mortgage interest, that your tenants are paying anyway, is deductible.

Not just if you itemize, either. The expenses all occur above the line, so you can take the standard deduction and still deduct all these expenses from your taxable rental income.

8. You Can Mitigate the Risks

The three major risks that landlords face are property damage, rent defaults, and vacancies. And you can mitigate every single one.

You mitigate property damage with tenant screening and security deposits. Rent defaults you mitigate with tenant screening and possibly rent default insurance. And vacancies you can minimize with a combination of tenant screening and proactive property management, maintenance, and advertising.

And, of course, you mitigate all three of those risks by buying properties in desirable markets, rather than high-crime, high-vacancy, lower-end markets that look good on paper.

Final Thoughts

Rental properties shouldn’t be your only retirement plan. But they can certainly help you reach financial independence faster and make an excellent supplementary source of income for retirement, especially early retirement.

They do require more work and education than stocks, both to buy and to manage. But if you’re willing to put in that work, to scale that barrier to entry, you can enjoy high yields, predictable returns, and ongoing income that keeps coming even as your net worth rises rather than erodes.

Follow Hashtags: #LindaCTurpin #AlbanyGARealEstate