Charles Koenig

Charles Koenig

In the midst of the current coronavirus-induced bear market, investors across the world have found themselves wondering what to do with their assets. Should they sell and cut their losses? Or if they have cash handy, should they buy assets while they’re down?

A global recession feels inevitable at this point, but no one knows how long it will last or how deep it will go. Every day seems to bring new (and mostly bad) news about the public health crisis due to COVID-19—and the economic fallout from shuttering businesses worldwide.

As both a real estate investor and a stock investor, I’ve been reviewing data from past recessions to get a sense of what’s in store this time around. Sure, my stock portfolio has been hammered. I’m having trouble completing renovations on a vacant rental property and worry about filling it with a reliable tenant in the midst of this mess.

But I’m also setting aside as much cash as I can to invest, because assets are on sale. And that window won’t stay open long.

First, a Brief Overview of Volatility

Stocks are extremely liquid; real estate is extremely illiquid. You can buy and sell stocks instantly, and for free. Real estate typically takes months to buy or sell and costs thousands of dollars to do so.

That lack of liquidity is typically a disadvantage in real estate versus other asset classes. But it comes with a huge perk as well—low volatility.

Because investors can buy and sell stocks instantly and at no cost, they do. Millions of transactions take place on stock exchanges around the world every single day. And each buy or sell order sends stock prices moving up or down.

We’ve now seen several days over the last month with double-digit stock index swings. Can you imagine nationwide home prices swinging by 11 percent in a single day? Of course not. Home prices move at a glacial pace compared to stocks because they’re so slow and difficult to transfer.

In an analysis of stocks versus real estate over the last 145 years, real estate saw half the price volatility compared to stocks. Given that volatility is a form of risk, it makes real estate an inherently less risky investment.

So how has real estate fared in recessions past, compared to stocks?

Real Estate in Recessions

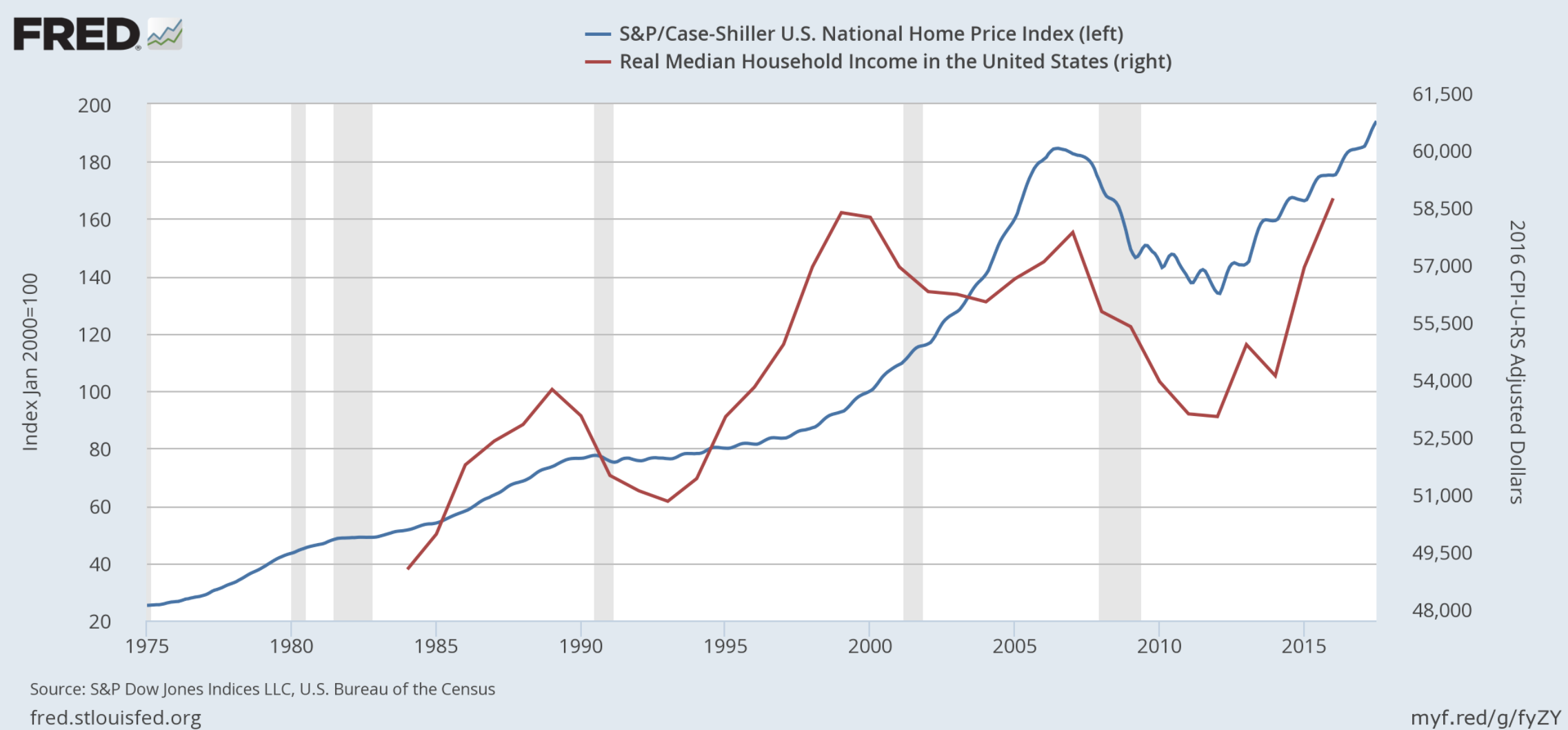

In most recessions, real estate has actually helped pull the U.S. economy out of the slide. Home prices typically flatten or slightly decline, developers stop building homes for a spell, and then demand catches up to the lack of new supply and suddenly buyers start driving up prices again.

Homebuilders get back to work, and Realtors, appraisers, title companies, lenders, furniture sellers, movers, and contractors all see a surge in business.

Take a quick look at this graph showing home prices since 1975, courtesy of Seeking Alpha:

The enormous exception, of course, is the Great Recession, which was largely caused by the housing market, making it a unique outlier (more on that later).

Stocks in Recessions

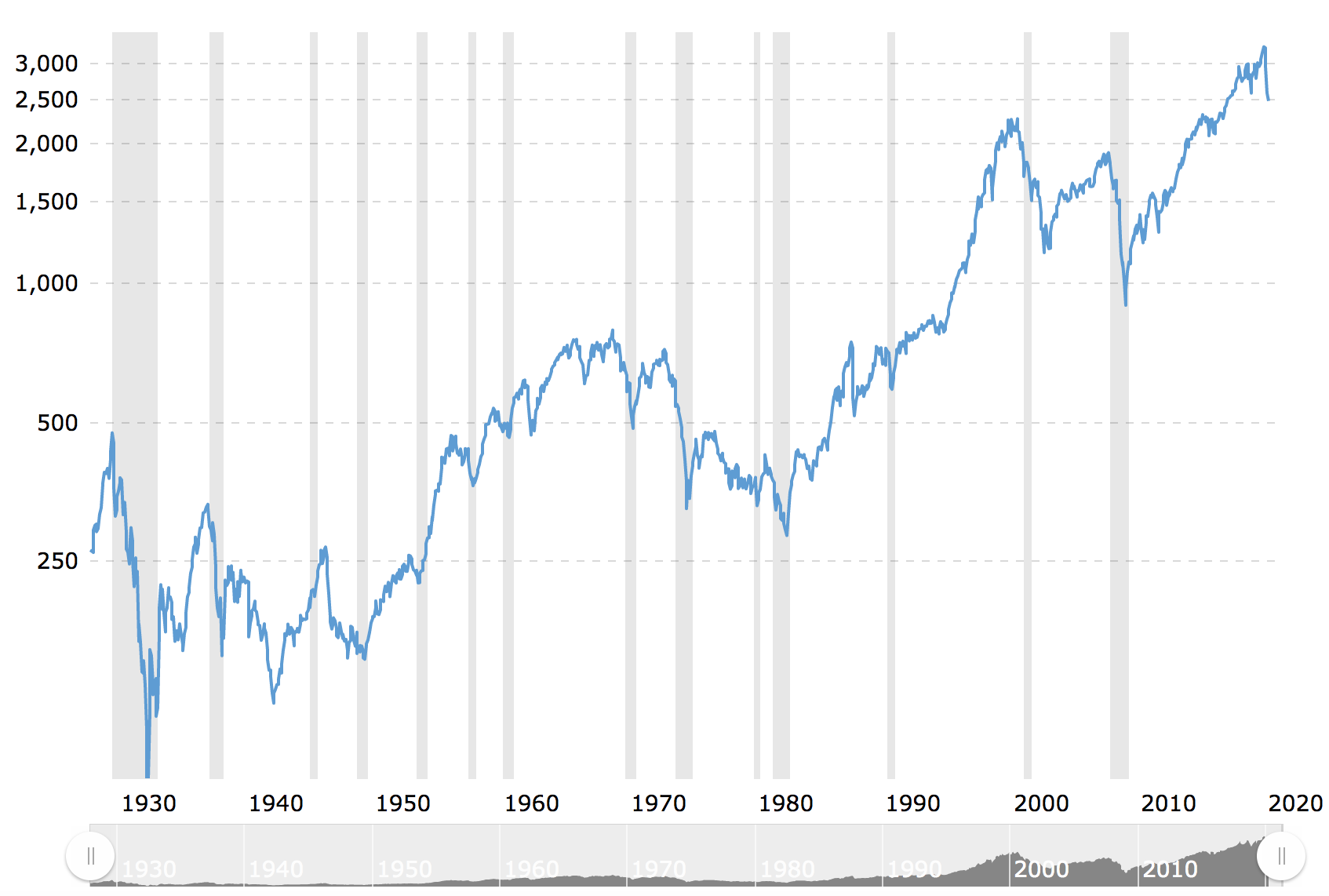

Stocks make for another story when recessions rear their ugly head.

In every single recession in U.S. history, stocks have fallen. No, not fallen—plummeted. See for yourself, in this graph of the S&P 500 courtesy of Macrotrends:

In some cases, the drop didn’t hurt too badly, while others were so bad that entire lifetimes of wealth disappeared. In the Great Depression, the S&P 500 fell by a terrifying 86 percent. More recently, in the Great Recession, the index fell by 54 percent.

Woof.

The Great Recession as a Housing Outlier

In the last recession, fueled in part by falsely-graded subprime mortgage derivative investments, U.S. home prices took a beating.

They had grown too high and too fast in the housing bubble of the mid-2000s. And they fell hard, toppling 33 percent from peak to valley—an enormous fall, a collapse even, by any calculation.

Yet that fall was still more than 20 percentage points fewer than the S&P 500 fall.

Think about it: Even in the one recession largely caused by real estate, home values still fell far less than stocks did.

Perhaps surprisingly, rents don’t tend to decline during recessions. Even during the Great Recession, they merely flattened for two years.

Why? Because demand for rental housing goes up as demand for homeownership pulls back.

Homeownership Rates and Stock Ownership Rates

The U.S. homeownership rate reached an all-time high in 2004 at 69.2 percent. It remained high until the housing bubble burst during the Great Recession and then fell to a 50-year low of 62.9 percent.

You remember the foreclosure wave—I don’t need to remind you. All those people became renters, at least temporarily, helping to buoy rents.

In the years since reaching that 50-year low in 2016, the homeownership rate climbed back up to 65.1 percent in the fourth quarter of 2019. And despite popular opinion, homeownership isn’t appropriate for everyone and comes with its own downsides. I’ve been a homeowner and I’ve been a renter, and they both have their pros and cons.

Stocks are another matter entirely—everyone should own some stocks, even if their asset allocation differs based on age, risk tolerance, and a dozen other factors. Yet lower- and middle-class Americans got spooked away from stocks in the aftermath of the Great Recession and had just barely started dipping their toes back in those waters again when the coronavirus ripped apart stock markets around the world.

In 2004, 63 percent of Americans owned stocks, according to a Gallup report. By 2013, that figure had fallen to 52 percent. Since then, it’s gradually edged back upward to a meager 55 percent. Get ready for it to fall again.

The problem is that lower- and middle-class Americans only get in on the action with stocks after they’ve already had a strong run, a charging bull market. Read—they buy high.

Then the market crashes and they panic and pull their money out of the market. Read—they sell low.

It is the wealthy who leave their stocks untouched during bear markets. And it is the wealthy who funnel more money into stocks when everyone else is screaming that the sky is falling.

Thus, it’s the wealthy who benefit most from the stock market recovery after a recession. Many point out how unfair it is, but the answer isn’t to empty the wallets of savvier investors. It’s to educate the lower and middle classes so they become savvier investors.

Final Thoughts

Ultimately, people still need housing—even in a recession. They may not be willing to go into as much debt to buy it, but demand for a roof over your head doesn’t go away. Some folks downsize, others sell their homes (at lower prices) and become renters. But demand doesn’t disappear, even as new supply stops being built.

But people don’t need to hold their stocks during recessions. They should, but they don’t. So stocks prices tumble, even as housing remains relatively steadfast.

I, for one, plan to buy as much real estate and stock as I can afford. Which granted, isn’t a lot right now, given the current crisis. But when others rush to sell, it’s usually a good time to buy.

Follow Hashtags: #LocalSocialPro